January 31 2023

1 Min Read

CLOs (Collateralized Loan Obligations) and CDOs (Collateralized Debt Obligations) sound similar but are fundamentally different.

CDOs gained notoriety for their detrimental role during the Great Financial Crisis (“GFC”) of 2007 to 2009. Since then, CDOs and CLOs have frequently been lumped into the same category. However, while “CLOs” and “CDOs” may rhyme, they are as different as AM and PM.

Today’s CLOs are nothing like the subprime CDOs of the past.

CDOs contributed to the GFC as a global conduit for the U.S. subprime mortgage and derivative meltdown.

According to a study by the Yale School of Management, Program on Financial Stability, “The primary catalyst that triggered the Global Financial Crisis (GFC) of 2007–09 was the market for subprime mortgage securities in the U.S. The engine driving the subprime surge … CDOs.”1

Financial institutions worldwide invested in U.S. subprime mortgages through CDOs in pursuit of higher yields. Ultimately, these institutions faced cataclysmic losses as U.S. home prices fell as a recession and higher unemployment rates impinged on the ability of many homeowners to pay their mortgages. Lax borrowing standards, minimal loan documentation, and even fraud exacerbated the problems with subprime mortgages. CDOs further magnified losses through leverage and derivatives.

“The primary catalyst that triggered the Global Financial Crisis (GFC) of 2007–09 was the market for subprime mortgage securities in the U.S. The engine driving the subprime surge … CDOs.”

Matthew Lieber and Steven Kasoff

Yale School of Management

In contrast, notes one author of the Yale study: “Collateralized Loan Obligations (CLOs), which use corporate debt instead of mortgages, performed well through the financial crisis; it remains a vibrant market today.”2

Market prices of CLOs declined in the depths of the GFC, but less than other securities.3 CLO market prices rebounded quickly when the markets and the economy recovered. Some CLO managers were even able to enhance profits by opportunistically trading underlying loans, selling weak credits, and buying undervalued securities amidst the volatility.

The strengths and structural protections of CLOs have led to the growth of the CLO market, with average annual issuance of $100 billion every year in the past decade. The global CLO market has grown steadily since the GFC and now exceeds $1 trillion.4 CLO investors—from conservative and risk-averse to aggressive and return-seeking—are able to select among varied CLO securities based on their particular risk-reward preferences.

“Collateralized Loan Obligations (CLOs), which use corporate debt instead of mortgages, performed well through the financial crisis; it remains a vibrant market today.”

Steven Kasoff

Yale School of Management

Preceding the GFC, the underlying collateral of CDOs was comprised primarily of subprime mortgages to consumers. Lax regulations in the mortgage market led to excessive lending with low underwriting requirements. Ultimately, these mortgages were securitized through CDOs. By 2006, over 50% of the mortgages held in CDOs lacked full documentation of borrowers’ income.5

Unfortunately, due to a recession, rising unemployment, and falling home prices, many homeowners were unable to afford their monthly payments. This “perfect storm” led to unraveling CDO markets, cashflow shortfalls in most CDOs, and high default rates across the CDO universe.

In addition, complex financial engineering increased the underlying risk of many CDOs. Notably, some CDOs allowed underlying collateral portfolios to include other CDOs as well as derivatives, such as credit default swaps on CDOs. (CDOs backed by other CDOs were called “CDOs squared.” CDOs backed by CDOs squared were called “CDOs cubed.” “CLOs squared” also existed, however cumulative loss rates across CLO tranches were nowhere near CDO levels.6) The leverage, layering, and complexity of “CDOs on steroids” exacerbated losses.

CDO losses during the GFC were significant. By 2009, CDOs comprised over half of the nearly one trillion dollars in losses suffered by financial institutions since the start of the crisis. At the time, more than half of the CDO tranches issued between 2005 and 2007 that were rated AAA fell to junk status or lost principal. Losses among AAA CDO tranches totaled $325 billion.7

Waves of legislation, regulation, and financial market reform followed the maelstrom caused by CDOs.

While CDOs faltered during the GFC, the CLO market demonstrated resilience.

“Standard and Poor’s found that AAA-rated tranches of CLOs issued before the 2008 crisis lost nothing,” write Wharton Professors Michael Roberts and Michael Schwert.8

Clearly, CLOs are discernibly different from CDOs.

“Standard and Poor’s found that AAA-rated tranches of CLOs issued before the 2008 crisis lost nothing.”

Prof. Michael Roberts

Prof. Michael Schwert

Wharton School, University of Pennsylvania

Underlying investments differentiate CDOs from CLOs. CDOs generally represent pools of consumer debt. CLOs represent pools of senior secured corporate loans.

In consumer debt pools like CDOs, there is a higher potential correlation of defaults across assets, significantly tied to unemployment rates. For households, the impact of a recession and higher unemployment is largely binary. Household breadwinners lose their jobs. Defaults on mortgages and other consumer loans may follow. As a result, consumer debt pools, backed by household wealth, are less diversified and highly correlated.

In contrast, senior secured corporate loan pools (like those collateralizing CLOs) benefit from mandatory borrower and industry diversification, generally better access to capital, and potential avenues for management flexibility during downturns.

In the face of a recession and a resulting decline in revenues, corporations can cut costs, staffing, and capital spending, and can shut plants. Businesses can lower their break-even levels and mitigate recession-induced declines in revenues and profitability. By contrast, households do not have these advantages.

In sharp contrast to CDOs derived from consumer debt, CLOs are collateralized by loans to large public and private companies within a highly regulated credit market. Moreover, CLOs generally invest in first-lien, senior secured loans. While these loans are generally rated BB or B, senior CLO tranches can earn investment-grade ratings due to their priority claim on cash flows from the underlying pools.

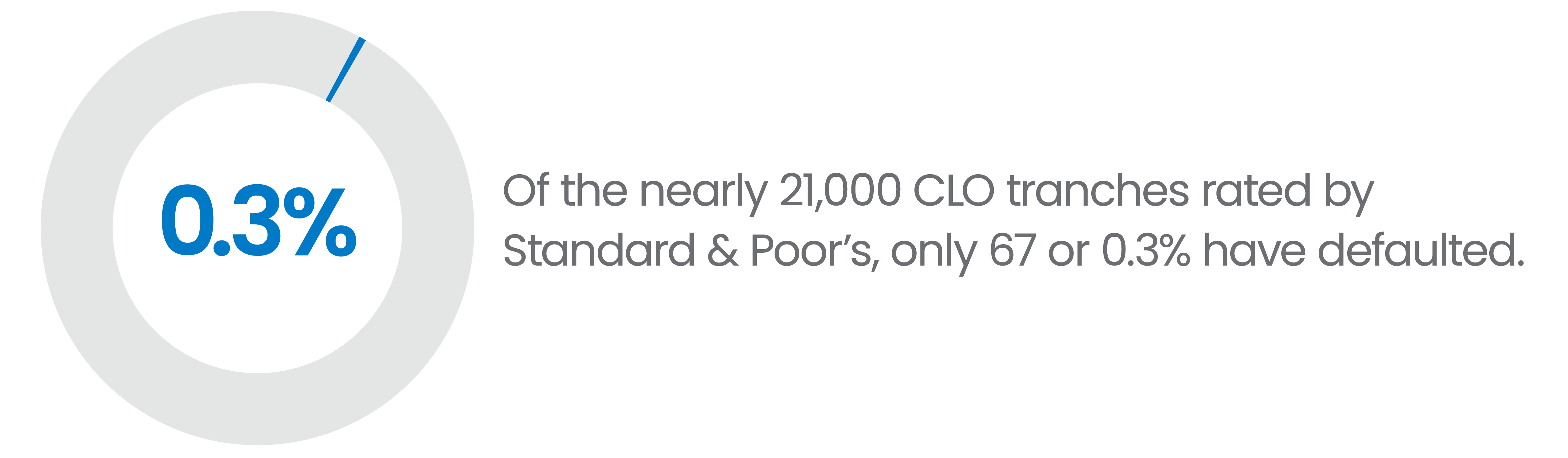

Unlike CDOs, CLOs have historically exhibited very few defaults. The largest and most senior CLO debt tranches (AAA-rated) have never experienced a default in the history of CLOs. Of the nearly 21,000 CLO tranches rated by Standard & Poor’s, only 67 or 0.3% have defaulted. Most of this small group of defaults were by tranches originally rated below investment grade.9

CLOs are created with a number of defensive characteristics.

CLO portfolios are typically diversified across 150 to 250 or more loans and dozens of industries. Contractually, exposure to any single industry is generally capped at 15% and exposure to any single company is generally capped at 2%. CLO managers are required to meet diversification requirements prescribed by a CLO indenture, which further helps to mitigate downside risk.

Across the CLO ecosystem, teams of credit analysts underwrite each individual loan in a CLO pool. CLO managers will continually assess a borrower’s credit quality, industry risk, and company risk, as well as macroeconomic conditions and regulatory headwinds to determine if a loan is suitable for their CLO portfolios.

Moreover, CLO documentation generally limits exposure to CCC-rated investments to no more than 5% to 7.5% of the pool. Post-GFC, more stringent industry practices and structural enhancements ushered in the era of CLO 2.0, eliminating high exposures to high-yield corporate bonds and limiting exposures outside of first-lien, senior secured loans.

CLO managers actively manage their loan portfolios on a daily basis and regularly reassess the health of their portfolios. CLO managers have the ability to trade their underlying loan portfolios to help maintain the credit quality of CLO pools and mitigate potential losses from loan defaults. Regular, comprehensive reporting provides transparency to CLO investors as holdings change.

The active management within CLOs is markedly different from other asset-backed securities, generally structured with static portfolios. Static portfolios provide investors with immediate visibility to underlying holdings, and prepayment speeds become the risk focus. However, static portfolios are vulnerable to collateral deterioration.

Under the terms of CLO indentures, managers must match the duration of the underlying loan portfolio to the duration of the CLO structure.

A series of coverage tests, mandated by covenants, govern CLOs. These required monthly tests measure the adequacy of the cash flows and the underlying loan collateral. These tests are designed to protect the viability of the CLO, with the highest level of protection provided to AAA and AA senior tranches.

If a CLO fails one of the tests, cash flow is diverted from the equity and lower-rated tranches to pay the interest and principal of the senior CLO tranches. After these payments sufficiently reduce the amount outstanding on the senior tranches, payments resume to the equity and mezzanine tranches. This process of “self-healing” is a unique structural protection of the CLO.10

The coverage tests above are non-mark-to-market and are based on cash flows, defaults, and the ratings quality of the underlying loans. This structure insulates CLO investors from short-term swings in loan prices and market volatility. Thus, CLOs do not become forced sellers of loans in market downturns. Rather, lower loan prices can present buying opportunities for CLO pool managers, who can capitalize on lower prices and higher spreads. Historically, wider reinvestment spreads can mitigate or exceed elevated loan losses during economic downturns. Reflecting this dynamic, total returns for CLOs rose in the years following the GFC.

With broad diversification and a wide variety of structural protections, CLOs have a robust performance history.

However, we must consider the impact of potential macro risks on the CLO market:

According to estimates by Wharton Professors Roberts and Schwert, loss rates would need to far exceed the 31% default rate seen in the Great Depression of the 1930s before the impairment of CLO collateral would impact investors in the largest, senior tranches.11 In comparison, leveraged loan default rates reached a record 10.8% in 2009; current default rates for leverage loans are under 1%.12 Moreover, CLOs comprise a small portion of the regulatory capital of banks and insurance companies.

Keep in mind that equity and junior tranches could see the suspension of interest payments and potential capital losses in a major economic downturn. However, junior and equity tranches largely endured and then prospered after the GFC and more recently after the Covid-19 downturn of 2020.

The systemic risk of CLOs, we believe, is not comparable to systemic risk exhibited by CDOs in 2007 to 2009.

“CLO” and “CDO” may rhyme, but the instruments are fundamentally different. We believe these differences make CLOs a compelling opportunity for income investors today. Most importantly, CLOs have demonstrated enduring performance across multiple market environments.

To learn more, reach out to us directly. We’d be pleased to answer your questions.

References

1. Matthew A. Lieber and Steven H. Kasoff, "Wall Street’s Subprime Debacle: Firsthand Accounts from Inside the CDO Machine," Journal of Financial Crises: Vol. 4: Issue 1, p. 371. (2022) https://elischolar.library.yale.edu/journal-of-financial-crises/vol4/iss1/11

2. Steven H. Kasoff, Yale School of Management Fellow, interview conducted and edited by Ted O’Callahan, “Inside the CDO Market That Catalyzed the Financial Crisis,” Yale Insights. (May 10, 2022) https://insights.som.yale.edu/insights/inside-the-cdo-market-that-catalyzed-the-financial-crisis

3. Morgan Stanley Research, CLO Primer page 52.

4. Leveraged Commentary & Data (LCD), as of December 31, 2022.

5. Sirio Aramonte and Fernando Avalos, “Structured finance then and now: a comparison of CDOs and CLOs,” BIS Quarterly Review. (September 22, 2019) https://www.bis.org/publ/qtrpdf/r_qt1909w.htm

6. Wells Fargo Securities, “CLO’s: How Bad Was it? CLO Market After Action Review: Part 1,” November 29, 2017, CLOs versus CDOs and CMBS – Five- and Ten- Year Loss Rates, Estimated Cumulative Loss Rates by Original Rating, 1993-2016.

7. Larry Cordell, Greg Feldberg, and Danielle Sass, “The Role of ABS CDOs in the Financial Crisis,” The Journal of Structured Finance, 25 (2) 10-27. (Summer 2019) https://jsf.pm-research.com/content/25/2/10.abstract

8. Michael R. Roberts and Michael Schwert, “Why Collateralized Loan Obligations Will Not Cause the Next Financial Crisis,” Knowledge at Wharton. (August 10, 2020) https://knowledge.wharton.upenn.edu/article/clos-will-not-cause-next-financial-crisis/

9. S&P Global, “Default, Transition, and Recovery: 2021 Annual Global Leveraged Loan CLO Default and Rating Transition Study.” (October 31, 2022) https://www.spglobal.com/ratings/en/research/articles/221031-default-transition-and-recovery-2021-annual-global-leveraged-loan-clo-default-and-rating-transition-study-12535652

10. Wells Fargo Securities, “CLO’s: How Bad Was It? CLO Market After Action Review: Part 1,” November 29, 2017

11. Roberts and Schwert, “Why Collateralized Loan Obligations Will Not Cause the Next Financial Crisis.”

12. Rachel Kakouris, “US loan default rate ends 2022 at 0.72%; downgrades, distressed volume in focus,” Pitchbook.com. (January 4, 2023) https://pitchbook.com/news/articles/us-loan-default-rate-ends-2022-at-072-downgrades-distressed-volume-in-focus

Check out our related posts based on your search that you may like