January 31 2023

1 Min Read

Collateralized Loan Obligations (CLOs) have historically offered a competitive risk/return profile.1

CLOs have achieved higher yields and total returns relative to many fixed-income securities with similar ratings.2 The floating rate nature of CLOs can offer additional returns and risk mitigation amidst rising rates and inflation.

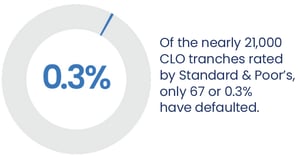

Moreover, CLOs have rarely defaulted, unlike other types of corporate debt and securitized products. The long-term default rate for CLOs is 0.3% according to S&P Global. Of the nearly 21,000 tranches rated by S&P since 1996, only 67 have suffered defaults, with no defaults among AAA tranches, the largest sector of the CLO market.3

What helps drive the resilience of CLOs?

A robust, “self-healing” structure and required monthly cash flow and collateral tests help insulate CLOs from a variety of risks.

To start, CLO managers must comply with multiple tests as they assemble the portfolio of senior secured loans that underly every CLO. Concentration tests require issuer and industry diversification. Quality guidelines limit the amount of low-rated securities. These tests help lead to stable, well-diversified, and high-quality loan portfolios. While underlying investments are primarily senior secured loans to large or middle-market U.S. corporations, they are below investment grade. The quality guidelines guide pool managers to higher-quality holdings with a lower risk of default. Since CLOs are actively managed, these quality guidelines help discipline the portfolio construction and management process.

The collateral quality tests work across multiple dimensions:

These quality tests help optimize the quality of CLO loan portfolios, reducing credit and default risk overall.

Once an underlying loan portfolio is constructed, monthly tests verify that the portfolio is able to make timely income and principal payments for the 8 to 12-year life of the CLO.

A series of coverage tests, mandated by indenture, govern the active management of a CLO. The required monthly tests measure the adequacy of the cash flows from the underlying loan collateral. The results of these tests can affect how cash flows are allocated among the various CLO tranches.

The interest and principal coverage tests work across multiple dimensions:

These internal tests also provide a “self-healing” or “self-correction” mechanism.

If a CLO fails either of the first two tests discussed above—the Interest Coverage Test or the Overcollateralization Test—cash flow is diverted from the equity and lower-rated mezzanine tranches to pay the interest and principal of the senior CLO tranches. After these payments sufficiently reduce the amount outstanding on the senior tranches, payments resume to the equity and mezzanine tranches. This process of “self-healing” is a unique structural protection of the CLO.

The third test—the Interest Diversion Test—requires that a portion of the interest is reinvested in additional loan collateral to strengthen and expand the amount of collateral supporting the senior tranches.

This monthly testing and “self-healing” process helps make CLOs resilient across market cycles.

These tests may lead to the temporary suspension of payments to affected CLO equity or CLO mezzanine debt. However, the self-correcting mechanism within the CLO structure helps support the strength of senior tranches and generally leads to the resumption of payments to these noteholders in the future.

We believe that the ongoing tests and resulting portfolio adjustments required to manage the loan portfolios of every CLO have improved historical results for the asset class.

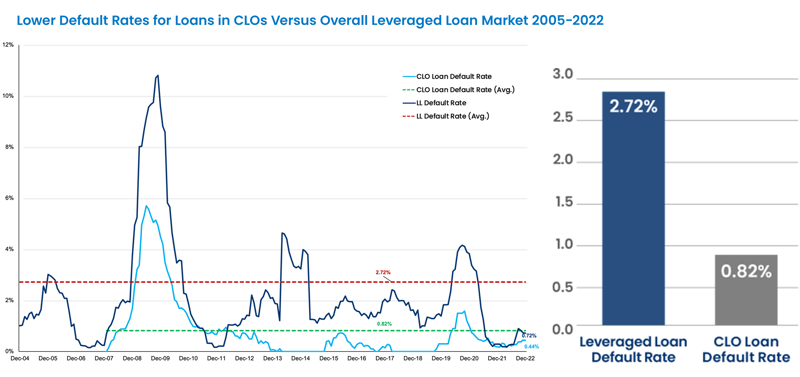

Notably, the default rates within CLO portfolios are lower than the default rates for the broader leveraged loan market, indicating the value of these tests and the importance of active management by CLO managers. While leveraged loans had an average long-term default rate of 2.72%, the loans within CLO loan portfolios had an average long-term default rate of only 0.82%.

Source: S&P LCD, Intex, Clarion, as of December 31, 2022.

We believe the robust structure and regularly required tests of CLOs have reduced risk and enhanced performance for CLO investors historically.

This helps explain why CLOs have grown into a $1+ trillion asset class over the past two decades.4

Are you exploring CLO investment opportunities? To learn more, read our FREE ebook:

“13 Powerful Benefits of CLOs for Today’s Income Investor (and 7 Risks to Know)”

1. Pinebridge, “Seeing Beyond the Complexity: An Introduction to Collateralized Loan Obligations,” January 19, 2022.

2. Wells Fargo Securities, “CLOs: How Bad Was It? CLO Market After Action Review Part 1,” November 29, 2017.

3. S&P Global, “Default, Transition, and Recovery: 2021 Annual Global Leveraged Loan CLO Default and Ratings Transition Study,” October 31, 2022.

4. Neuberger Berman, “Global CLO Market Hits $1 Trillion Milestone,” August 2021.

Check out our related posts based on your search that you may like