January 31 2023

1 Min Read

Sophisticated investors have increased their allocations to alternative investments in recent years in pursuit of higher octane returns and differentiated results. Alternative strategies in private credit, private equity, and hedge funds have attracted significant assets from diverse investor types, including taxable high-net-worth investors.

However, taxable investors in alternatives face an unpleasant surprise when they review their K-1s at tax time. They are confronted with the inevitable implications of “phantom income”. These investors discover they must pay taxes on investment gains that have not yet been realized through a cash sale or a distribution. They must also pay taxes on gross, pre-fee returns, not net returns and are paying taxes on the portions of returns that went into management fees.

Why are management fees not deductible? In 2017, Congress passed the Tax Cuts and Jobs Act (TCJA). The TCJA eliminated or reduced many deductions. As a result, investment management fees were deemed non-deductible for tax years 2018 to 2025.1 These amounts can be significant for investors with large allocations to alternatives.

But there is a solution for investors confronted by tax implications from problems like phantom income: Insurance Dedicated Funds (IDFs), only available within private placement life insurance and variable annuities (PPLI and PPVA). By investing in IDFs through PPLI and PPVA, investors can relieve themselves from significant tax implications and enhance compound returns.

The TCJA signaled the end of miscellaneous itemized deductions and the deductibility of investment management fees. For most investors, investment management fees and expenses were considered to be miscellaneous itemized deductions. For tax years prior to 2018, such deductions could be included on Schedule A of a taxpayer’s Form 1040. These deductions were commonly called “2% Floor Deductions” because a taxpayer needed miscellaneous itemized deductions in excess of 2% of their Adjusted Gross Income to deduct these expenses. Many sizeable investors exceeded this threshold.

One of the nation’s premier experts on the taxation of alternative investments (the late Robert Gordon) called the repeal of this deduction a “perfect storm” for taxable investors in hedge funds.2 The clouds of this perfect storm cast a shadow on alternative investments, particularly those strategies generating significant short-term capital gains or interest income, including private credit. The resulting “phantom income” attributable to non-deductible investment management fees can create significant tax liabilities and lower net after-tax returns.

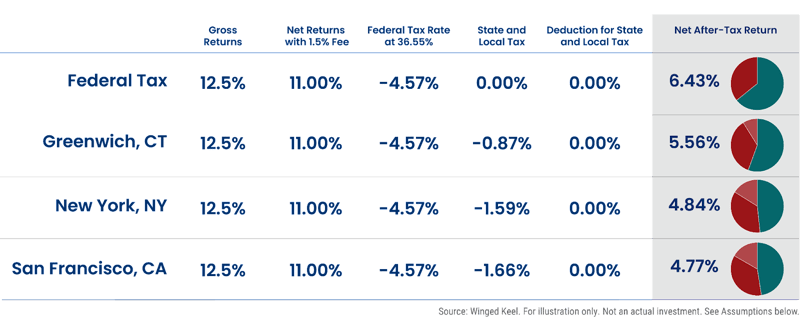

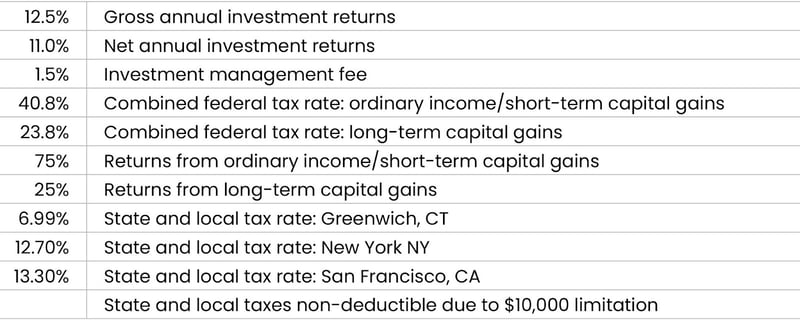

Hypothetical Illustration

Fortunately, there is a solution to the problem of high taxes on alternative strategies, as well as the non-deductibility of investment management fees: Insurance Dedicated Funds or “IDFs.” Sophisticated taxable investors can invest their alternative allocations through IDFs for relief from current taxation and compound their capital at higher rates while deferring taxes.

IDFs offer access to alternative strategies such as private credit, private equity, and hedge funds, as well as other high-yield or high-turnover investment products. IDFs also offer simplified tax reporting without the need for complicated K-1s.

Structurally, IDFs are commingled investment vehicles open only to the separate accounts of insurance carriers and annuity providers. Qualified individuals, businesses, and institutions (generally with $5 million or more of investable assets to comply with securities law) can access IDFs only through PPLI or PPVA. As commingled vehicles, IDFs can only accept subscriptions from life insurance companies.

Importantly, PPLI and PPVA provide low-cost institutional pricing compared to retail insurance products, leading to even greater compounding.

There is over $2 trillion worth of variable life insurance and variable annuities currently receiving tax-efficient treatment under U.S. tax law.3 Earnings within these insurance-related products are generally not subject to current taxation, and life insurance benefits payable to beneficiaries are generally exempt from income tax and even estate tax in certain cases. To be eligible for these tax benefits, policies must be properly structured and implemented.

Are you searching for a tax-efficient approach to alternative strategies? Looking for relief from the problem of phantom income from the non-deductibility of investment management fees?

Insurance Dedicated Funds (IDFs) offer a compelling option for tax-efficient investing. By thoughtfully incorporating IDFs into your clients’ investment portfolios, you can unlock the potential for enhanced compound returns.

To learn more, download our FREE guide:

“Advisor’s Roadmap to Insurance Dedicated Funds”

1. Ebony J. Howard, CPA, “Are Financial Advisor Fees Tax Deductible?”, Annuity.org, updated April 27, 2023, https://www.annuity.org/financial-advisors/are-financial-advisor-fees-tax-deductible/

2. Robert Gordon, “Hedge Funds Taxation: A Perfect Storm Ahead,” Investments and Wealth Monitor, May/June 2019, https://investmentsandwealth.org/getattachment/1abddef5-5e4e-4468-8e3e-3d38ff107013/IWM19MayJun-HedgeFundsTaxation.pdf

3. Jonas Katz, “Insurance-Dedicated Funds 101: Growth, Trends and Next Steps,” SALI Fund Services, 2022, https://www.sali.com/uploads/2022/09/8456cb74485c7aa7d4123ea20e2a4da4/sali-fund-services-insurance-dedicated-funds-101.pdf

Check out our related posts based on your search that you may like